New Lease Standard and Impact to Not-For-Profit Organizations

In February 2016, the Financial Accounting Standards Board ("FASB”) issued Accounting Standards Update No. 2016-02, Leases (codified as Accounting Standards Codification (“ASC”) Topic 842). This new standard seeks to increase transparency and comparability among organizations, including not-for-profits, by recognizing rights and obligations of leasing activities as assets and lease liabilities on the balance sheet.

Key Provisions of the New Standard

Topic 842 brings most operating leases onto the lessee balance sheets. Previously, only capital leases (referred to as “finance leases” under the new standard) were required to be recognized on lessee balance sheets. The main changes are as follows:

- Nearly every lease will be recognized on the balance sheet. Lessees will report a lease obligation and a corresponding right-of-use asset for both operating and finance leases, measured at the present value of lease payments.

- Contracts with a non-cancelable term of less than 12 months might not qualify for the short-term lease exception if an entity is reasonably certain that renewal options will be exercised.

- Lessor accounting is largely similar to previous guidance, with a few minor modifications. Lessors will continue to classify leases as either sales-type, direct financing, or operating.

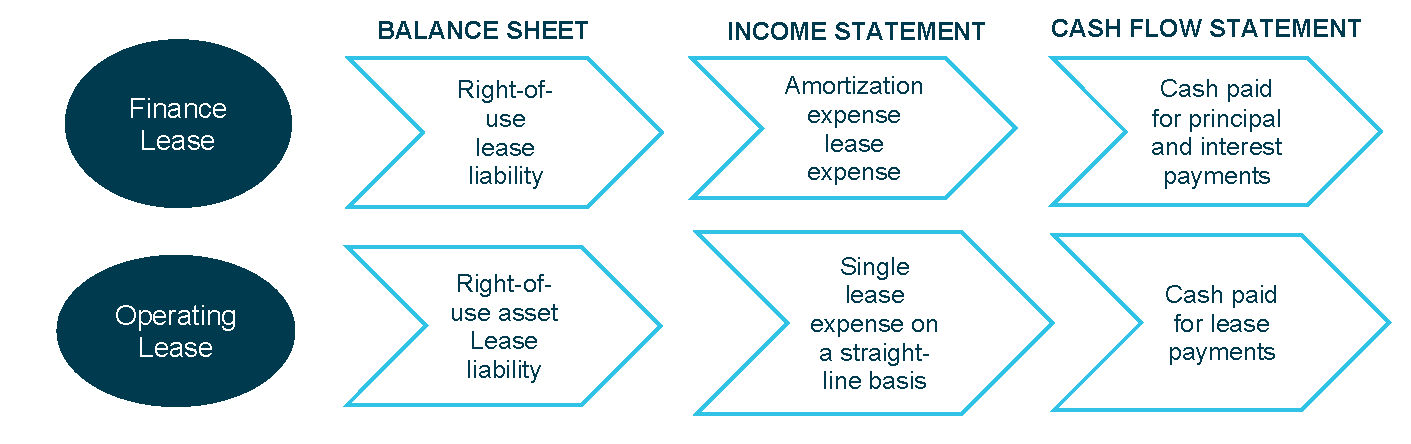

Lessee accounting treatment has been updated as follows:

Components of a Contract

Topic 842 requires entities to identify the lease components, non-lease components, and other items that are not considered contract components. Identifying these elements is important because consideration in the contract is allocated only to the lease and non-lease components. Although this requirement does not differ from that under existing U.S. GAAP, the effect of not applying this requirement correctly under Topic 842 is more significant because most leases must be recognized on the balance sheet under the new guidance.

Non-lease components are distinct elements of a contract that are not related to securing the use of the lease asset. Arrangements that include both lease and non-lease components are common in real estate transactions.

For example, a real estate lease in which the lessee pays for both the use of the space (lease component) and common-area maintenance services (non-lease component). The consideration allocated to the lease component is accounted for under Topic 842, while the consideration allocated to the non-lease component is accounted for under other relevant GAAP.

Leases (ASC 842) – Lease and Non-Lease Components

Disclosure Requirements

The new lease standard significantly increases the required lease disclosures. Not-For-Profits should take the disclosure requirements into consideration early on to ensure they understand them and are prepared. The objectives of the disclosures is to enable financial statement users to assess the amount, timing, and uncertainty of cash flows arising from leases.

Implementation Challenges

Not-for-Profit organizations may face some challenges with the implementation of the new lease standard including:

- Identifying and locating leases. Not-for-profit organizations need to reevaluate each existing lease, both old and new contracts, and determine whether they fall under the new definition. Extracting lease information can be a significant undertaking, especially to those that have large volume of arrangements. A formal inventory of all lease arrangements should be conducted. Furthermore, a review of the general ledger for rent expense, accounts payable ledgers, vendor and customer contracts, financials, and other relevant documents is strongly recommended.

- Setting up a leasing system. Many not-for-profit organizations currently rely on Excel spreadsheets to track the leases. This may still be a viable option under the new lease standard for entities with minimal and simple lease arrangements. However, for those with numerous and complex leases, this practice might not be the most efficient way to process all calculations and track the lease terms and other relevant lease information completely. Due to the accounting complexities and disclosure requirements of the new standard, the use of a more advanced system may need to be considered.

- Modifying policies and procedures relating to leases. Many still think that the lease accounting under the new standard will only be handled by the finance team. More often than not, copies of lease agreements are kept and maintained by departments outside of the financeteam. Modifying policies and procedures to align them with the requirements of the new standard is crucial. Organizations should review or create a policy for handling new lease contracts so that these are carefully evaluated, entered into a lease system, tracked, and reported.

- Debt covenant compliance. Since almost all leases will be on the balance sheet, relevant debt covenants (i.e., debt-to-equity ratios) may be negatively impacted. For not-for-profit organizations with debt that includes financial covenants, a preliminary analysis of the impact must be assessed. Communication with lenders and third parties ahead of time to explain the expected impact and the reason behind it can help avoid non-compliance. In certain circumstances, such timely communication may also assist in rewriting of agreements or addendums prior to the computation.

Transition and Effective Date

How We Can Help

With all the presentational and disclosure changes involved with the new lease standard, the key is to start the identification process early. Citrin Cooperman has a dedicated team of not-for-profit professionals available to help you get started with your implementation.

Related Insights

All Insights

Our specialists are here to help.

Get in touch with a specialist in your industry today.