Supplier finance programs (SFPs), which also may be referred to as reverse factoring, payables finance, or structured payables arrangements, have become a game-changer in the manufacturing and distribution (M&D) industry, revolutionizing cash flow management and strengthening buyer-supplier relationships. As M&D companies increasingly adopt these programs, it becomes crucial to understand and navigate the accounting complexities they present.

Supplier finance programs

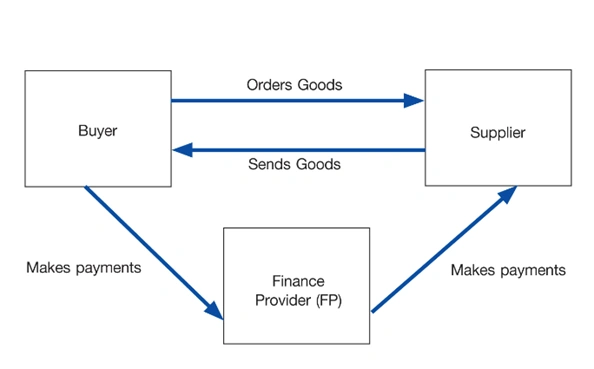

In a typical SFP arrangement, the buyer (often a large company) partners with a finance provider (FP), usually a bank, to offer its suppliers the option to receive early payment for their outstanding invoices. Instead of waiting for the agreed-upon payment term, suppliers can choose to sell their invoices to the FP at a discount. The FP then pays the supplier the discounted amount, providing them with immediate working capital. The objective of the process is to empower both buyer and seller with control over cash flow, fostering a spirit of collaboration rather than emphasizing negotiation.

The following illustration created by The CPA Journal depicts a basic SFP arrangement:

Now that we have a basic knowledge of what SFPs are, we will discuss the various accounting considerations and best practices associated with SFPs in the M&D industry.

Classification and presentation

One of the common questions that arises in a SFP activity is regarding its proper classification in the buyer’s financial statements. Should the liability for goods and services purchased from a supplier in the ordinary course of business and initially paid by an FP in a SFP arrangement be shown as an “accounts payables” or “short-term debt?”. It is important to appropriately classify these liabilities on the balance sheet. Designating the portion of payables subject to early payment arrangements separately from regular accounts payable provides for clear visibility into the impact of early payment arrangements on working capital and financial obligations. Misclassifying liabilities as trade payables or financial liabilities can impact key financial ratios and distort the understanding of the company’s liquidity and leverage.

Enhancing disclosure requirements

Proper classification and presentation of SFP transactions are vital for transparent financial reporting. Companies should distinguish between regular accounts payable and payables subject to the program. Disclosures should include the nature, terms, and potential financial effects of the program on the company’s financial statements. Robust disclosures provide stakeholders with a clear understanding of the program’s significance and its impact on financial performance. Inadequate or misleading disclosures can result in legal and regulatory non-compliance, investor dissatisfaction, and reputational damage.

To improve the transparency and disclosures of SFP transactions, on September 29, 2022, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update 2022-04, Liabilities – Supplier Finance Programs (subtopic 405-50): Disclosure of Supplier Finance Program Obligations, to enhance the transparency about the use of SFP for investors and other allocators of capital. The amendments in ASU 2022-04 require that a buyer in a SFP disclose sufficient information about the program to allow a user of the financial statements to understand the program’s nature, activity during the period, changes from period to period, and potential magnitude. To achieve that objective, the buyer should disclose qualitative and quantitative information about its SFP. The amendments in ASU 2022-04 are effective for fiscal years beginning after December 15, 2022, including interim periods within those fiscal years, except for the amendment on roll-forward information, which is effective for fiscal years beginning after December 15, 2023. Early adoption is permitted.

Internal controls

Establishing strong internal controls is vital to effectively manage the accounting and financial aspects of SFP. Companies should implement processes to ensure accurate recording and reporting of program transactions, adherence to accounting policies and standards, and prevention of fraudulent activities. Regular monitoring and evaluation of controls provides assurance that financial reporting is reliable and that the program operates in accordance with established policies and procedures.

Collaboration with stakeholders

Accounting professionals should collaborate closely with stakeholders, including procurement, treasury, and external financial providers, to ensure proper accounting treatment and alignment of objectives. Cross-functional collaboration promotes accurate financial reporting, transparency, and effective management of the SFP.

Other considerations

The Securities and Exchange Commission (SEC) staff has suggested that companies consider making disclosures in management’s discussion and analysis (MD&A) if the effects of a SFP are material to current-period liquidity or are reasonably likely to materially impact liquidity in the future. SEC registrants should consider the SEC staff guidance on SFP to determine whether they need to provide disclosures in MD&A.

Supplier finance programs offer immense potential for improving cash flow management and fostering stronger buyer-supplier relationships. However, navigating the accounting landscape associated with these programs is crucial for accurate financial reporting and compliance. By carefully considering the classification, recognition, and disclosure requirements, and establishing robust internal controls, finance professionals can effectively leverage supplier finance programs to optimize working capital while maintaining transparency and adherence to accounting standards. Collaboration and communication with stakeholders further enhance the success of these programs, supporting a sustainable and thriving supply chain ecosystem.

Citrin Cooperman’s Manufacturing and Distribution Industry Practice’s team provides professional services and industry insights to assist our clients in achieving their business goals. If your business is interested in exploring the benefits of a supplier finance program, please contact your Citrin Cooperman advisor.