Current Economic Environment provides ‘Perfect Storm’ for Wealth Transfer and Associated Tax Savings

The current tax law allows for the transfer of wealth in ways that can minimize the impact on estate taxes. 2020 presents an opportunity to do so at unprecedented levels. What does that mean? It means the lifetime federal estate and gift tax basic exclusion or “exemption” is $11.8 million per individual and $23.6 million per couple. Thus, an individual or couple can transfer assets totaling $11.8 million and $23.6 million, respectively, without paying any estate or gift tax which can amount to 40% of the transferred fair market value.

While this exemption is not scheduled to revert back to 2017 levels until 2026 (i.e. $5.5 million per individual and $11.0 million for couples), 2020 may be the most beneficial time to take advantage of this opportunity. A change in leadership in the upcoming election in November could put the magnitude and timeline of the current exemption at risk and diminish the ability to transfer wealth tax free.

One could argue that pairing the current economic and financial environment, due to the COVID-19 pandemic (the “Pandemic”), with the threat to the wealth transfer exemption makes 2020 the most certain time to take advantage of this enormous tax savings opportunities.

While the exemption limit is law, and the political outcome uncertain, what makes the current valuation environment favorable for estate planning and wealth transfer? The current economic and financial environment has led to extreme uncertainly for businesses, companies, and organizations. Uncertainty inherently increases risk, which in turn leads to lower values of assets, securities, businesses, and real estate. This provides an opportunity for more assets to be transferred and less of the exemption to be utilized.

To determine the amount of assets eligible for transfer, one must retain a qualified valuation professional to determine the fair market value of said assets. The IRS defines fair market value as:

“the price at which the property would change hands between a willing buyer and a willing seller, neither being under any compulsion to buy or to sell and both having reasonable knowledge of relevant facts.” 1

It is important to consider how a business or asset is valued. In most cases one or more of the three approaches to value, the Income Approach, the Market Approach and/or the Cost or Asset Approach, is employed. While each approach has a multitude of methods, each approach has a basic theoretical premise that is impacted by the current economic environment.

The Income Approach is based on the premise of expectation, or what would a hypothetical buyer would expect to extract from a business in the future and what would they pay for those benefits in today dollars? The application of this approach requires the determination of a subject asset’s representative earning power, which is then discounted at a rate to bring those future dollars back to a present value. The application of the discount rate to future cash flows is designed to capture

the risk associated with those cash flow materializing in the future. The riskier the cash flows the higher the discount rate and the lower the value. Thus, businesses or assets whose income streams are less certain or expected to be lower, or a combination of both, are likely to have a lower value than when those income streams that were more certain and more robust prior to the Pandemic.

The Market Approach on the other hand is based on the premise of substitution, where an investor compares the value of other alternatives to determine the fair market value price to pay for a specific business or asset. In most cases the comparable investments considered are publicly traded businesses or comparable private and public company transactions in similar industries and financial positions as the subject company or asset. The multiples or ratios of value to a specific economic measure such as Revenue, EBITDA, or Earnings, of the comparable business or transaction are used as a benchmark in valuing private assets and businesses.

The current environment has halted much merger and acquisition activity making the employment of private company transaction multiples difficult. However, the public market is telling a compelling story as it relates to value. To gauge the general market impact the Pandemic, albeit not exclusive, has had on the pricing multiples of publicly traded companies, we reviewed how common stocks were being priced by the market as of December 31, 2019 relative to April 30, 2020 relative to their last twelve months (“LTM”) revenue and earnings before interest, tax, depreciation, and amortization (“EBITDA”).

We analyzed ten primary industries as presented in S&P Capital IQ using the following search parameters:2

- Traded on U.S. Major Stock Exchange (Primary);

- Positive 2019 EBITDA; and

- Analyst coverage greater than 10 analysts.

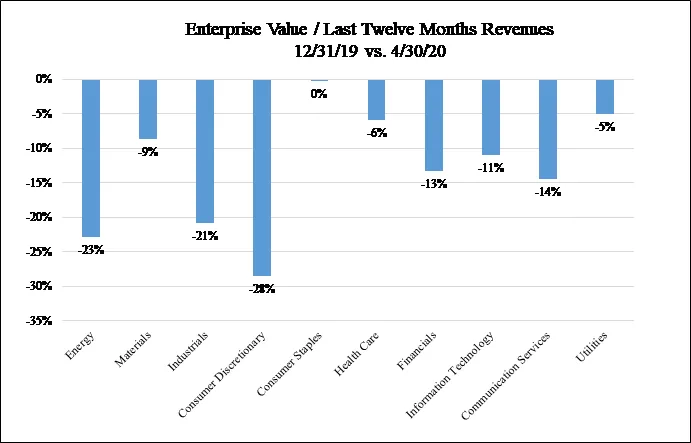

The following graph demonstrates the relative change in revenue pricing multiples as of December 31, 2019 relative to April 30, 2020 across ten industries.

This chart was created with data points from S&P Capital IQ.

As indicated in the preceding graph, the pricing of the Consumer Staples and Utilities industries relative to revenues have been the least impacted by the Pandemic with Consumer Staples unchanged and Utilities experiencing a decrease of 5%. The pricing of the Consumer Discretionary and Energy industries relative to revenues have been hit the hardest decreasing 28% and 23%, respectively.

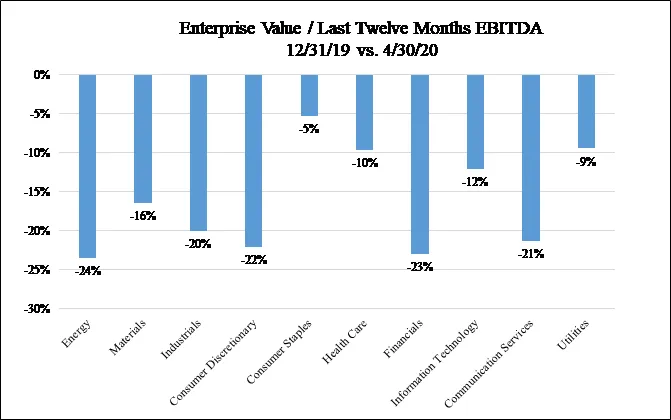

The following graph demonstrates the relative change in EBITDA pricing multiples as of December 31, 2019 relative to April 30, 2020 across ten industries.

This chart was created with data points from S&P Capital IQ.

As indicated in the preceding graph, the pricing of the Consumer Staples and Utilities industries relative to EBITDA have been the least impacted by the Pandemic with a decrease of 5% and 9%, respectively. The pricing of the Energy, Consumer Discretionary, and Financial industries relative to EBITDA have been hit the hardest with all decreasing in excess of 22%.

Even the Cost or Asset Approach, which is most pertinent where a company’s value is tied directly to the value of its underlying assets, assumes the assets of a business less liabilities recasted at their market value equals fair market value. If the underlying assets are securities, real estate, or other market driven assets, the current economic environment is likely to lead to lower values compared to pre-Pandemic levels. This combined with higher debt borrowing at the current low interest rates would net a lower equity value.

When planning 2020 gifts it is important to consider the timing of these transfers. In performing an appraisal, the appraiser should consider what is known or knowable as of the valuation date. The Statement on Standards for Valuation Services No. 1 issued by the American Institute of Certified Public Accountants (“SSVS No. 1”) provides the following commentary in regards to the valuation date:

“The specific date at which the valuation analyst estimates the value of the subject interest…Generally, the valuation analyst should consider only circumstances existing at the valuation date and events occurring up to the valuation date.”

Transfers in 2020 should consider what was known or knowable as of that date. The exact valuation “cutoff date” as to when the pandemic should be considered is not clear and is at the discretion of the valuation analyst. The table below provides a summary of noteworthy developments regarding the birth, evolution, and spread of the Pandemic.3

|

Date |

Event |

|

December 31, 2019 |

Chinese Health officials informed the World Health Organization ("WHO") about a cluster of 41 patients with a mysterious pneumonia. |

|

January 7, 2020 |

Chinese authorities identified the virus that caused the pneumonia-like illness as a new type of coronavirus. |

|

January 11, 2020 |

China recorded its first death linked to the novel coronavirus. |

|

January 13, 2020 |

The first coronavirus case outside of China was reported in Thailand. |

|

January 20, 2020 |

The first US case was reported. |

|

January 30, 2020 |

WHO declared a "public-health emergency of international concern." |

|

February 14, 2020 |

Europe's first death tied to the outbreak reported in France. |

|

February 21, 2020 |

The number of COVID-19 cases spiked in Italy. |

|

February 29, 2020 |

The US confirmed its first death from COVID-19 on American soil. |

|

March 3, 2020 |

Coronavirus cases began to sharply increase in Spain. |

|

March 11, 2020 |

WHO declared the outbreak a pandemic; US banned all travel from 26 European countries. |

|

March 13, 2020 |

A US national emergency was declared over the novel coronavirus outbreak. |

|

March 23, 2020 |

New York City became the epicenter of the coronavirus epidemic in the US. |

|

March 26, 2020 |

The US leads the world with 82,404 confirmed cases. |

|

March 31, 2020 |

More than one-third of humanity came under some form of lockdown. |

Based on the events outlined in the preceding table, it does not seem practical to consider the impact of the Pandemic for valuation dates in the calendar year 2019. That being said, when in 2020 is the “correct date?” Two events occurred on March 11, 2020: (1) the WHO declared the outbreak a pandemic and (2) the US banned all travel from 26 European countries. This was followed by a declaration of a national emergency in the US on March 13, 2020.

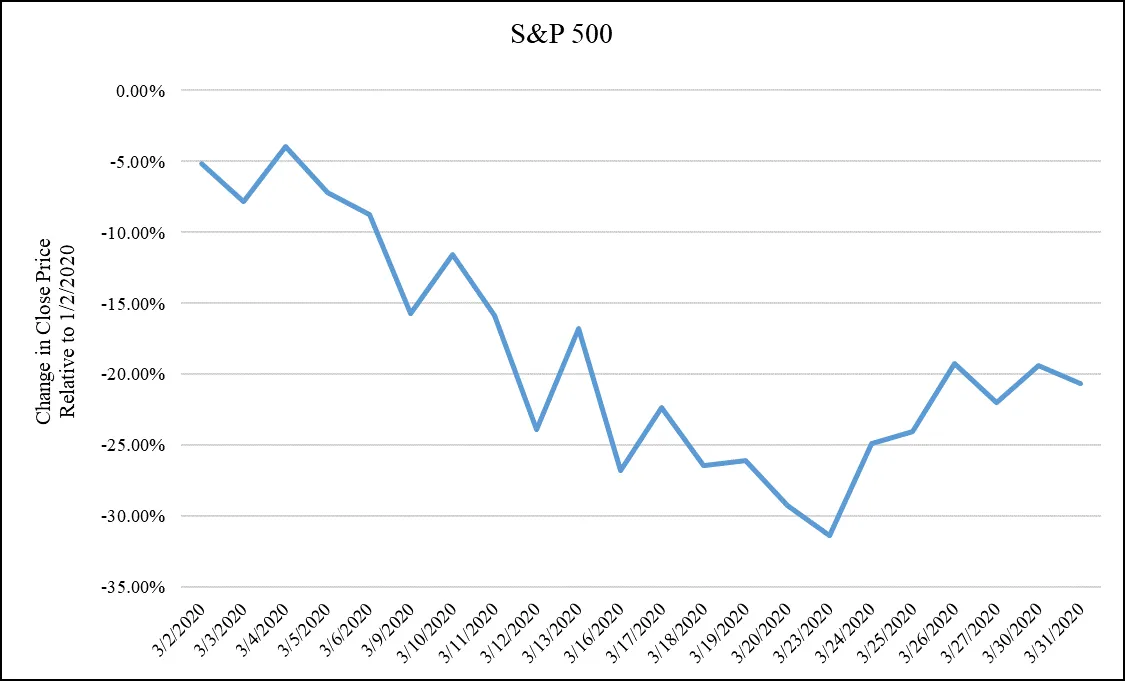

Recognizing that valuations are highly dependent on market driven inputs, we analyzed the reaction of the investing public to what was predominantly due to news surrounding the Pandemic by a review of the close price of the S&P 500 index throughout the month of March 2020 relative to the close price on January 2, 2020, as illustrated in the following graph.4

This chart was created with data points from S&P Capital IQ.

As of March 12, 2020, the S&P 500 was down nearly 24% relative to January 2, 2020 demonstrating the market “understood” the severity of the pandemic.

Taking the timeline of events and market reaction as illustrated by the S&P 500 into account, coupled with the fact that valuation standards require valuation analysts to value companies based on what was known or knowable as of a specific date, it seems reasonable for analysts to consider the impact the Pandemic for valuation dates of companies on or about March 12, 2020, with exceptions of course.

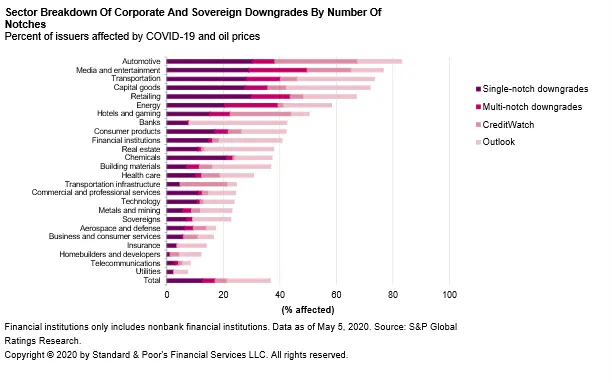

We also considered if certain industries were more impacted than others. To gauge the general market impact, albeit not exclusive (e.g. oil prices and other factors), the Pandemic has had on specific industries, we analyzed the percentage of companies that have experienced corporate and sovereign credit downgrades across 25 sectors of the economy. See the following graph for data compiled as of May 5, 2020.

As indicated in the preceding graph, the automotive, media and entertainment, transportation, capital goods, and retailing sectors have experienced the highest percentage of downgrades with all exceeding 60% of industry operators being affected. The utilities, telecommunications, homebuilders and developers, and insurance sectors have been the least impacted which does not come as a surprise as these businesses are “essential” to the economy.

The impact of the Pandemic on companies and industries as well as the current financial and economic conditions suggest an environment of lower valuations for assets, securities, and businesses. While valuation may be uncertain in the current environment, the potential for a turnaround or sudden appreciation for many, if not all, assets and business is a potential reality to be considered when contemplating wealth transfer.

If a transfer of such assets has been contemplated, now is the time to act. The combination of lower valuations, the high exemption threshold, and the potential for one or both to change after the fall of 2020 makes this the right time to consider and make such transfers where feasible.

1Source: Internal Revenue Service, Treasury Regulation §20.2031-1.

2Real Estate has been excluded due to inadequate sample size.

3“A comprehensive timeline of the new coronavirus pandemic, from China's first COVID-19 case to the present,” by Holly Second, Aylin Woodward and Dave Mosher, Valuation Products and Services, April 7, 2020.

4Based on data retrieved from S&P Capital IQ.

Related Insights

All InsightsOur specialists are here to help.

Get in touch with a specialist in your industry today.